The labor budget Direct is used to calculate the number of man hours that will be required to be able to produce the units specified in the production budget.

It is prepared after the production budget is drawn up, because the budgeted production figure in units provided by the production budget serves as the starting point in the direct labor budget..

Changes in actual sales can directly affect production budget and direct labor estimates. The number of employees that need to be scheduled on the production line is based on these figures..

The budget provides information at an aggregate level. Therefore, it is not normally used for specific hiring and firing requirements. Shows the total cost and number of direct labor hours required for production.

A more complex labor budget will calculate not only the total number of hours needed, but will also break this information down by job title. It is generally presented in a monthly or quarterly format.

Article index

It is useful for forecasting the number of employees that will be needed to staff the manufacturing area throughout the budget period. This allows management to forecast hiring needs. Likewise, when to schedule overtime and when layoffs are likely to occur..

Helps management plan their workforce requirements. The labor budget is a component of the master budget.

Creating a sales budget helps determine labor needs. This is because this information is used to develop the production budget..

The production requirements established in the production budget provide the starting point for preparing the labor budget..

The labor budget takes the estimated production figures in order to estimate the direct labor cost. This information allows you to decide how many employees are needed on the production line..

In addition to employee salaries, all other employee expenses are included in the labor budget.

Included expenses are worker's compensation insurance, Social Security contributions, unemployment taxes. Also life and health insurance premiums where applicable, pension plan contribution and many other employee benefits.

Generally, employee-related expenses vary based on their salaries. However, some of these expenses are fixed amounts..

A company must choose how it plans to account for employee benefit expenses, both budgeted and actual.

These expenses are included in the cost of direct labor, or are considered as general expenses of the employee, being assigned to the units produced. However, sometimes these expenses are treated as a period expense..

The method by which these variable employee expenses are accounted for will have an impact on the cost of merchandise sold, revenue, or inventory budgets..

In cases where direct labor constitutes a large part of variable expenses, this difference will be significant..

The direct labor budget can be controlled by external forces, the unions being the most important among them..

Generally, there is an increase in the cost of direct labor when the old labor contract is terminated and the new contract is initiated..

Additionally, technological advances that require a change in the production process may require changing the skill level of employees. Hiring employees with higher skill levels affects the workforce budget.

Creating a detailed labor budget may be found to be too time consuming when there are a large number of job classifications. This is because it is extremely difficult to match budgeted salary levels with real world workforce..

The basic calculation used by the budget to calculate direct labor requirements is to import from the production budget the expected number of units produced for each period and multiply it by the standard number of labor hours for each unit..

Direct labor hours to meet production requirements are multiplied by the average direct labor cost per hour. In this way the total budgeted direct labor cost is obtained.

The amount of labor hours required to produce each unit is calculated. All departments that handle the product during production are included.

This produces a subtotal of the labor hours required to meet the production target. More hours can also be added to account for production inefficiencies. This would increase the number of direct work hours.

For example, a toy requires the cutting department, sewing department, and finishing department to require a total of 0.25 hours per unit.

Employees should be observed in the work they do on the products and the handling time of the units of each department to establish the required production time.

To obtain the average cost of labor per hour, the different hourly rates are added and the result is divided by the number of rates used.

For example, suppose labor wages are $ 11, $ 12, and $ 13 per hour. These amounts are then added together to get $ 36. This amount is then divided by 3, giving an average labor cost of $ 12. This is the average hourly wage.

This estimated cost is calculated by multiplying the number of hours per unit by the average labor cost per hour. In the example, it would be 0.25 hours times $ 12 per hour, equivalent to $ 3 per unit. The direct labor cost would be $ 3 for each unit produced.

The labor cost per unit is multiplied by the total number of units planned to be produced. For example, if 100,000 units are planned to be produced, then the cost will be $ 3 per 100,000 units. This gives a total labor cost of $ 300,000.

The total labor costs are divided into monthly costs. For each month, how many units are planned to be produced is projected and multiplied by the cost of labor per unit.

- Automatic consideration is given to the time factor. This is because normally the wages paid are proportional to the time worked.

- Labor rates are more stable than material prices.

- Certain variable overheads vary to some extent with the number of workers employed. Therefore, the production charge is related to the amount of wages paid. This amount is proportional to the number of workers.

- The basic data required for the calculation of this rate is readily available from the wage analysis statement and does not involve additional labor costs..

- No distinction is made between skilled and unskilled work, with their respective differences in pay rates. This is unfair, since it is the unskilled workers who are responsible for higher expenses, in the form of material waste, depreciation, etc..

- If workers are paid on a piece-rate basis, then the time factor is completely ignored.

- No distinction is made between the production of manual workers and that of workers who operate machines.

- The method gives an incorrect result when workers receive an overtime bonus, as higher hourly rates are paid for work during overtime.

- No distinction is made between fixed and variable expenses.

- When labor is not an important factor of production, the absorption of overheads will not be equitable. Ignores important factors such as the widespread use of plants and equipment.

- It is not suitable in the case of piece workers, since the same rate will be applied to absorb the general expenses of all workers, they are efficient and take less time or they are inefficient and take more time.

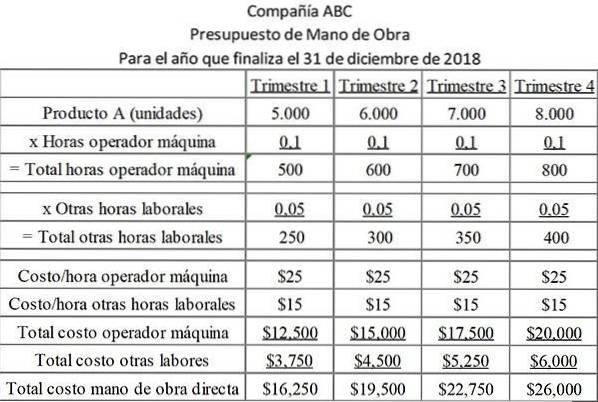

The ABC company plans to produce a series of plastic cups during the budget period. The vessels are all within a limited size range. Because of this, the amount of labor involved in processing each one is almost identical..

The work path for each cup is 0.1 hours per cup for the machine operator, and 0.05 hours per cup for the rest of the job. The labor rates for machine operators and other personnel are substantially different. Therefore, they are recorded separately in the budget..

The following table shows the hours required for each job category by quarter, as well as the cost of each type of job.

The budget contains two types of labor that are grouped separately as they have different costs.

0.1 machine hour is required for each product manufactured, costing the company $ 25 per hour. In addition, an additional 0.05 hour of time is required for each product manufactured. This costs the company $ 15 per hour..

Yet No Comments