The Cash register It is a process that is generally executed in businesses such as supermarkets, restaurants and banks, carried out at the close of the business day or at the end of a cashier's shift. This accounting process makes the cashier responsible for the money in their cash register..

Even with today's modern point of sale systems, a procedure is still needed to account for a store's cash receipts. These internal controls are necessary to prevent money mismanagement and to safeguard assets against loss or theft..

Strong internal controls not only promote operational efficiency, but also ensure reliable accounting records, which will be needed when filing taxes..

One of the most common causes of reduction or losses in a store is due to poor handling of cash. When investigated, the most common cause is a lack of proper procedures or controls.

Article index

At the beginning of each shift, each teller must be assigned their own cash drawer. Have the cashier count the cash in the drawer to verify the opening balance.

You want to keep a constant amount of money in the box. This ensures that you will always have enough cash to give change to customers..

The next step in keeping your safe is to make cash deposits throughout the day. Depending on the volume and number of transactions, the amount of deposits to be made will vary..

After determining when this deposit will be made, the cash is counted and the difference is subtracted from the initial morning count. Cash register for a cash register is generally done at the end of the day or at the end of a cashier's shift.

The cash drawer and its contents should be taken to an office or other isolated area to prepare the report. This is the time to make sure the money that came in and went out during the day was done efficiently and honestly..

As you prepare to count money, all large bills, checks, and food stamps are pushed aside and set aside..

The total amount in the till is counted first, including checks and credit card income. After finishing adding the amounts, this figure is manually compared with what the point of sale system shows.

After the drawer returns to its initial allotted amount, it is placed in the safe or handed over to another cashier who is starting their shift. Now, bills and change that were put aside along with checks from the cashier's box are counted.

This is what makes up the cashier's sales deposit. Most cash registers can print a sales receipt and a money receipt receipt. These receipts indicate how much the cashier made in sales and how much money was posted.

If the amounts match, everything is fine. Otherwise, a little more scrutiny will have to be done..

Consider having two people to arch the boxes. One person will count the drawer and create the daily cash report, while the other will prepare the bank deposit.

Both people must sign the report, stating their responsibility for the figures shown. Although no system can prevent fraud, this audit trail will help discourage complicity among employees..

When a discrepancy occurs, the money is counted again to ensure that the amount is correct.

Any excess and / or shortage should be investigated. Small discrepancies are common and generally caused by human error, possibly the cashier counting change for a customer. The largest discrepancies should be observed more closely.

Frequent discrepancies can be a sign of theft from an employee, or indicate that more training is required for a particular teller.

The over / under can always be calculated by subtracting the amount of money in the drawer, excluding the initial amount, from the amount printed on the cashier's receipt..

Depending on the amount of over / under and the circumstances involved, disciplinary measures may vary. Cashiers have lost their positions due to overruns / shortages, whether due to repeated violations or large overruns or shortages.

The shortages are usually due to bills sticking together, the cashier giving back too much in change, or maybe even pocketing some money.

Leftovers are produced by taking too much money from customers or by not correctly entering items in the point of sale terminal.

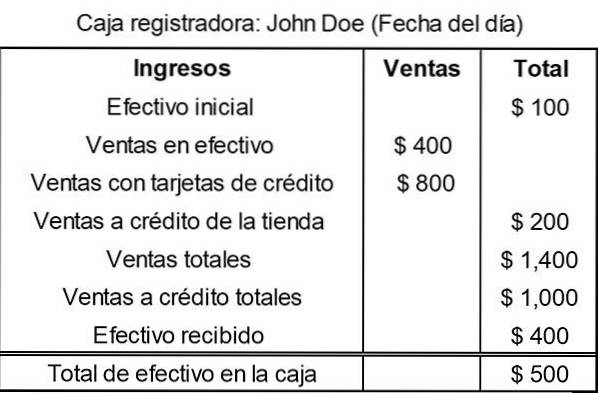

At the Omega store, the cash register process actually begins at the end of the day before, when cashier John Doe and his manager accept the amount of cash left in John's cash register..

When John comes to work the next morning, he starts with the amount of money that was left in the box. At the end of each business day, he or his manager posts a summary of the day's activity at the cash register, thus generating a report of the total sales made by the cashier..

To do this, John counts the amount of cash in his till, as well as check totals, credit card income, and store credit sales. Then fill out a form like this:

The manager checks the amount actually produced by John's box, and compares it with the form made.

If the amount of cash in the box does not match the form, the manager and John will seek to identify the error. If it cannot be found, a cash over / under form will be filled out.

Some companies charge the cashier directly for any shortage. Others take the position of firing the teller after a certain number of shortages for a certain amount of money. For example, three missing more than $ 10.

The store manager decides how much cash to check out or check in for the next day. It does this task for each of the tellers. Then bank all the cash and checks for the day in a nightly deposit box.

The manager then sends a report with the details of the deposit to the accountant to enter the data into the accounting system..

Yet No Comments