The journal entries They are the transaction records that are part of the accounting journal. Therefore, they are used to record commercial transactions in the accounting records of a company..

They can be posted to the general ledger, but also sometimes to a subledger, which is then summarized and moved to the general ledger. The general ledger is used to create the financial statements of the business. As a result, the journal entries will directly change the account balances in the general ledger..

In manual or automated accounting systems, business transactions are first recorded in a journal. That's where the term journal entries come from..

They are an important part of accounting. They can consist of several records, each of which will be a debit or a credit. The total of the debits must be equal to the total of the credits, otherwise it will be said that the journal entry is "unbalanced".

Journal entries can record one-time items or recurring items, such as depreciation or bond amortization.

Article index

Journal entries are the first step in the accounting cycle and are used to record all business transactions in the accounting system..

As business events occur throughout the accounting period, journal entries are posted to the general journal to show how the event changed the accounting equation.

For example, when the company spends cash to purchase a new vehicle, the cash account is reduced or credited, and the vehicle account is increased or debited..

The logic behind a journal entry is to record every business transaction in at least two places, known as double-entry bookkeeping..

For example, when a cash sale is generated, this increases both the sales account and the cash account. Purchasing products on credit will increase both the accounts payable account and the inventory account..

Journal entries, and their accompanying documentation, should be archived for several years, at least until it is no longer necessary to audit the company's financial statements..

The minimum retention period for journal entries should be included in the corporate filing policy.

Computerized accounting systems automatically record most business transactions in general ledger accounts.

They do this immediately after they have prepared sales invoices, write checks for creditors, process customer receipts, etc..

Therefore, you will not see journal entries for most business transactions, such as customer or vendor invoices. Journal entries are not used to record high volume activities.

In accounting software, journal entries are generally entered using separate modules, such as accounts payable, which has its own subledger, indirectly affecting the general ledger..

However, some journal entries will need to be processed to record transfers between bank accounts or accounting adjustment records..

For example, you probably have to make a journal entry at the end of each month to record depreciation. This entry will contain a debit in depreciation expenses and a credit in accumulated depreciation.

Also, there will likely be a journal entry to accrue the interest on a bank loan. This entry will contain a debit in interest expense and a credit in interest payable..

A manual journal entry that is posted in the general journal of a company will consist of the following items:

- The corresponding date.

- The amounts and accounts that will be debited.

- The amounts and accounts that will be credited.

- A short description or note.

- A reference, such as a check number.

These recorded amounts, which will appear in the journal ordered by date, will be posted to the general ledger accounts.

Journal entries are generally printed and stored in an accounting transaction folder, with accompanying supporting materials supporting such entries..

Thus, external auditors can access this information as part of their year-end audit of the company's financial statements and related systems..

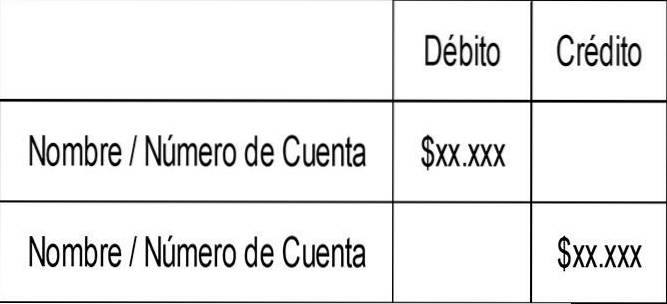

The detailed structure for writing a journal entry in the accounting is indicated as the following:

- A header line, which can include a journal entry number and a journal entry date.

- The first column contains the account number and the name of the account in which the journal entry is recorded. This field will have an indentation if it is for the account that is being credited.

- The second column contains the debit amount to be entered.

- The third column contains the amount of credit to be entered.

- A footer line can also contain a short description of the reason for the entry.

Thus, the basic journal entry record entry format is presented as follows:

The structural rules of a journal entry are that there must be a minimum of two items on two different lines in the journal entry, and that the total amount entered in the debit column must equal the total amount entered in the credit column..

An adjusting journal entry is used at the end of the month to be able to modify the financial statements and thus comply with the relevant accounting framework, such as Generally Accepted Accounting Principles or International Financial Reporting Standards..

For example, unpaid wages could accrue at the end of the month if the company is using an accrual basis of accounting..

A composite journal entry is one that includes more than two lines of entries. Often used to record complex transactions, or multiple transactions at the same time.

For example, the journal entry for recording a payroll generally contains many lines, as it involves the recording of numerous tax liabilities and payroll deductions..

Typically this is an adjusting entry that is reversed at the beginning of the next period. It usually happens because an expense should have accrued in the previous period, but is no longer necessary.

Therefore, the accumulation of wages in the previous period is reversed in the following period, to be replaced by a real payroll expense.

Yet No Comments