The trial balance or verification is an accounting report where the amounts of the balances of all accounts in the general ledger of a company are collected. Debit balances are listed in one column and credit balances in another column. The total of these two columns must be identical.

A company prepares a trial balance generally at the end of each reporting period, in order to ensure that the entries in a company's accounting system are mathematically correct..

The asset and expense accounts appear in the debit column of the trial balance, while the liability, principal, and income accounts appear in the credit column..

It should be run on a regular basis. This helps to quickly identify any problems and fix them as soon as they arise. Trial balance preparation should be tied to the company's billing cycle.

Article index

The preparation of a trial balance for a company serves to detect any mathematical errors that have occurred in the double entry accounting system.

If the total of debits is equal to the total of credits, the balance of the test is considered balanced and there should be no mathematical errors in the accounting books.

However, this does not mean that there are no errors in a company's accounting system. For example, transactions that have been classified incorrectly or those that are simply missing from the system could be major accounting errors that would not be detected by the trial balance..

The trial balance is not a financial statement. It is primarily an internal report that is useful in a manual accounting system. If the trial balance is not "balanced," this indicates an error somewhere between the journal and the trial balance..

Often the cause of the difference is a miscalculation of an account balance, accounting a debit amount as credit (or vice versa), incorporating digits into an amount when posting or preparing the trial balance, etc.

If all the accounting entries were fully recorded and all the general ledger balances were drawn accurately, the total of the debit balances that appear on the trial balance should be equal to the addition of all the credit balances.

- It is the first phase to prepare the financial statements. It is a working instrument used by accountants as a platform for the preparation of financial statements.

- Guarantees that for each debit record entered, the corresponding credit record has also been entered in the books, in accordance with the concept of double-entry accounting.

- If the trial balance totals do not match, the differences may be investigated and resolved prior to preparing the financial statements..

- Ensures account balances were accurately drawn from ledgers.

In a trial balance worksheet, all debit balances form the left column and all credit balances form the right column, with the account names placed at the far left of the two columns..

All open ledger accounts in the chart of accounts are listed by account code.

The total debits and credits for each general ledger account are listed. You should have a table with four columns. The columns should be: account code, account name, debit and credit.

For each open ledger account, its debits and credits are added for the accounting period in which the trial balance is running. The totals for each account are recorded in the appropriate column. If the debits and credits are not the same, then there is an error in the general ledger accounts.

If you find that you have an unbalanced trial balance, that is, the debits are not equal to the credits, then you have an error in the accounting process. That error has to be found and corrected..

After listing all the general ledger accounts and their balances on a trial balance sheet in their standard format, all debit and credit balances are added separately to demonstrate equality between total debits and total credits.

Such uniformity ensures that there are no unequal debits and credits that have been entered incorrectly during the double-entry registration process..

However, a trial balance cannot detect accounting errors other than simple mathematical errors..

If equal debits and credits are entered into wrong accounts, or a transaction is not posted, or offset errors are made at the same time with a debit and a credit, the trial balance would show a perfect balance between the total debits and credits.

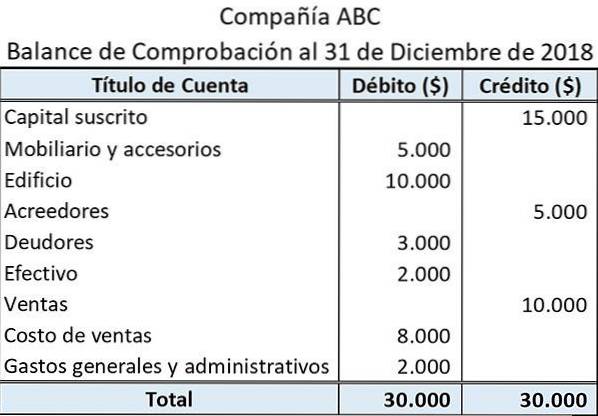

Here's an example of what a simple trial balance looks like:

The title provided at the top shows the name of the entity and the end of the accounting period for which the trial balance was prepared..

The account title shows the names of the ledgers from which the balances have been drawn.

Balances related to assets and expenses are presented in the left column (debit side). On the other hand, those related to liabilities, income and equity are shown in the right column (credit side).

The sum of all debit and credit balances is displayed at the bottom of their respective columns.

The trial balance only confirms that the total debit balances agree with the total credit balances. However, the trial balance totals may match despite any errors that may have occurred..

An example could be an incorrect debit entry that is offset by an equal credit entry.

Similarly, a trial balance does not provide any proof that certain transactions have not been posted at all. In such a case, the debit and credit aspects of a transaction would be omitted. This would cause the trial balance totals to still be in line.

Yet No Comments