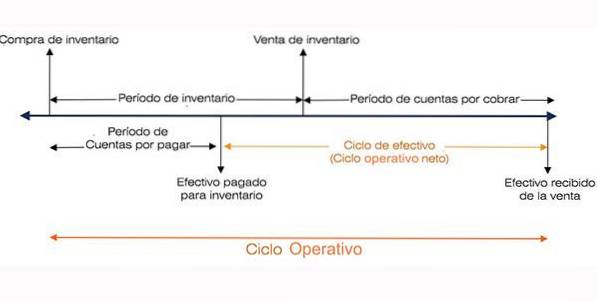

The operating cycle refers to the days it takes for a business to receive inventory, sell that inventory, and collect the cash from the sale of that inventory. This cycle plays an important role in determining the efficiency of a business's performance..

The operating cycle makes use of accounts receivable and inventory. It is often compared to the cash conversion cycle, because it uses the same component parts.

However, what makes them different is that the operating cycle looks at these components from the perspective of how well the company is managing operating capital, rather than the impact these components have on cash..

It is called the operating cycle because this process of producing / buying inventories, selling them, recovering cash from customers, and using that cash to buy / produce inventories, is repeated while the company is operating..

The operating cycle is useful for estimating the amount of working capital that a company will need to maintain or grow its business. Another useful measure used to evaluate the operational efficiency of a company is the cash cycle.

Article index

A company with an extremely short operating cycle requires less cash to maintain its operations, so it can still grow and sell at relatively small margins.

Conversely, if its operating cycle is unusually long, a company can be profitable and still require additional financing in order to grow, even at a moderate pace..

The operating cycle is a measure of the operational efficiency and the management of the working capital of a company. A short duty cycle is good. This will indicate that the company's cash is tied up for a shorter period.

The operating cycle is often confused with the net operating cycle. This is also known as the cash cycle. The net operating cycle indicates how long it takes for a business to collect cash for the sale of inventory.

On the other hand, the operating cycle is the period of time between the purchase of the inventory and the cash collected from the sale of the inventory..

The net operating cycle is the period of time between the payment of the inventory and the cash collected for the sale of the inventory.

The operating cycle offers a vision of the operational efficiency of a company. A shorter cycle is preferred, as this indicates a more efficient and successful business.

A shorter cycle indicates that a company will be able to quickly recoup its investment and have enough cash to meet its obligations. If a company's operating cycle is long, this indicates that the company needs more time to convert its inventory purchases into cash..

It's easy to assume that shorter is better when it comes to a company's cash conversion cycle or operating cycle. This is true in the case of the first, but not necessarily the case in the second.

Of course, there are many variables linked to managing accounts receivable, inventory, and accounts payable. These variables require many decisions to be made by managers.

For example, short collection times can restrict sales. Minimum inventory levels can mean that a business cannot fulfill orders in a timely manner. This is likely going to result in some lost sales..

Therefore, it appears that if a company is experiencing strong growth in sales and reasonable earnings, the components of its operating cycle should reflect a high degree of historical consistency..

The consistency of these indices in the history of a company is one of the most important measures of success.

The formula used to calculate an operating cycle in days is as follows:

Duty cycle = RI + RCC, where

RI = Inventory turnover.

RCC = Turnover of accounts receivable.

Inventory turnover is equal to the average number of days a company sells its inventory.

On the other hand, the accounts receivable turnover is the period of days in which the accounts receivable are converted into cash..

Alternatively, the following expanded formula can also be used to calculate the operating cycle:

Operating Cycle = (365 / Cost of Merchandise Sold) × Average Inventories + (365 / Credit Sales) × Average Accounts Receivable.

To determine the operating cycle of a business, analysts must first calculate the various components used in the above formula.

Once the amounts of inventory turnover and accounts receivable turnover are in place, they can be included in the formula, to determine the operating cycle of a company..

-The cost of merchandise sold, available in the annual income statement of a company, must be divided by 365 in order to find the amount of the cost of merchandise sold per day.

-Calculate the average inventory amount by adding the inventory amount at the beginning (or end of the previous year), and the ending inventory amount. Both amounts are available on the balance sheet.

Then divide by 2 to get the average amount of inventory for the time period in question..

-Divide the average amount of inventory obtained in step 2, by the amount of the cost of merchandise sold per day, obtained in step 1.

For example, a company with a cost of merchandise sold of $ 760 million and an average inventory of $ 560 million will have an IR as follows:

$ 730 million / 365 = $ 2 million (cost of merchandise sold per day).

RI = $ 560 million / $ 2 million = 280 (inventory turnover days).

The RCC can be calculated using the amounts of net sales and accounts receivable, with the following steps:

- Divide net sales, available in a company's annual income statement, by 365 to determine the amount of net sales per day.

- Calculate the average amount of accounts receivable, adding the initial amount (or ending of the previous year) and the final amount of accounts receivable. Then divide by 2 to get the average over the time period in question.

- Divide the average amount of accounts receivable by the amount of net sales per day.

It is common to also express the two main components of the operating cycle (RI and RCC) as a factor of (x) times, in terms of business volume.

Thus, an inventory turnover of 280 days would be expressed as a turnover of 1.3 times per year. This is because 365 days / 280 days = 1.3 times.

Some analysts prefer the use of days as it is more literal and easier to understand from a conceptual point of view.

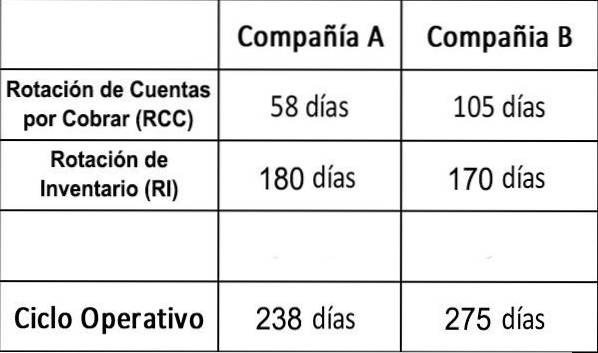

We can compare two hypothetical companies, Company A and Company B, with the following figures:

In terms of the collection of accounts receivable, the RCC figures show that company A is significantly more efficient operationally than company B.

Common sense would determine that the longer a company has uncollected money, the greater the level of risk it assumes..

Is Company B negligent in not collecting its accounts receivable more efficiently? Or maybe you are trying to increase your market share by allowing your customers more attractive payment terms?

These two companies have almost the same inventory in days. In this case, both companies have IR figures that are higher than the average for one company across all industries..

This, then, is likely a reflection of the industry in question, rather than poor efficiency. However, to get a more complete picture, it would be useful to compare these two IR figures with those of other companies in the same industry..

In a sense, A is more efficient at using other people's money, but from these numbers alone the reason for this is not immediately clear..

An analyst is likely to want to know what that means for the creditworthiness of each of these companies and why they are different..

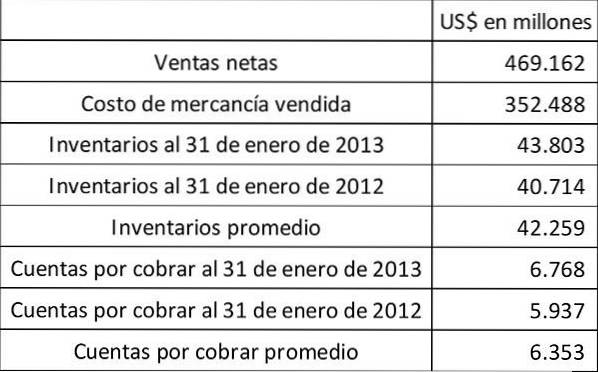

Walmart Stores Inc. has a lot to do with inventories. We will find your operating cycle assuming that all your sales are: (a) cash sales, and (b) credit sales.

Days taken to convert inventories to accounts receivable = 42,259 / (352,488 / 365) = 43.76.

Since there are no credit sales, the time required to recover cash from accounts receivable is zero. Customers always pay cash immediately. Therefore, the operating cycle in this case is: 43.76 days.

There is no change in the days taken for the conversion of inventories to accounts receivable.

Days taken to convert accounts receivable into cash = 6,353 / (469,162 / 365) = 4.94.

In this case, the operating cycle is: 43.76 + 4.94 = 48.70.

These values should be compared to the operating cycle of Walmart's competitors, such as Amazon, Costco, and Target..

Yet No Comments