The absorbent costing, Also called total absorption costing, it is a managerial accounting costing method that charges all costs related to the manufacture of a specific product. This method involves using the total direct costs and overhead costs associated with manufacturing a product as the cost basis..

Direct costs associated with making a product include the wages of the workers who directly make the product, the raw materials used to make the product, and all overhead, such as utility costs used to make a product. product.

Absorbing costing is also called total cost, since all costs - including overhead - are included as product cost..

Unlike the other alternative costing method, called direct costing, overhead is allocated to each product manufactured, regardless of whether it is sold or not.

Article index

- Absorbing costing involves the distribution of overhead costs among all units produced in a given period. Instead, direct costing groups the sum of all overhead expenses and reports that expense as a separate line..

- Determine a unit cost of overhead to be assigned to products.

- It is different from the other costing methods in that it also takes into account fixed manufacturing expenses (such as plant rent, utilities, depreciation, etc.).

- Absorbing costing will result in two categories of overhead: those applicable to the cost of merchandise sold and those applicable to inventory.

The cost estimate is assigned to the batch product (a non-repeating set of multiple production units).

The cost calculation is assigned to the product in a systematic way, since there are no batches.

The calculation of the cost assigned to the final product is taken from all cost and expense items.

- Absorbing costing takes into account all production costs, not just direct costs, as direct costing does. Includes the fixed costs of running a business, such as salaries, facility rental, and utility bills.

- Identify the importance of fixed overhead costs involved in production.

- Shows less fluctuation in net profit in case of constant production, but with oscillating sales.

- It creates a unique situation in which, by manufacturing more units, the net income is increased. This is so because overheads are distributed among all units manufactured; overhead per unit will decrease in cost of merchandise sold as more items are produced.

- As assets remain part of the company's books at the end of the period, absorbing costing reflects fixed costs assigned to items within ending inventory..

One of the main advantages of choosing to use absorbing costing is that it complies with Generally Accepted Accounting Principles (GAAP) and is required to report to the Internal Revenue Service (IRS).

Even if a company chooses to use direct costing for its internal accounting purposes, it still has to calculate absorbing costing to file taxes and issue other official reports..

It will result in more accurate accounting with respect to ending inventory. In addition, more expenses are accounted for on unsold products, which reduces the actual expenses reported. This results in a higher net income being calculated when compared to the direct costing calculation..

They give the company a more accurate picture of profitability than direct costing, if products are not sold during the same accounting period in which they are manufactured.

It can be important for a company that increases its production long before an expected seasonal increase in sales..

The use of absorbing costing could be particularly critical for small companies that often lack financial reserves. These companies cannot afford to make losses or sell products without having an idea of accounting for overhead..

It is difficult to take into account all the fixed manufacturing overheads to calculate the price per unit to assign to the products.

- It can make a company's level of profitability appear better than it is in a given accounting period, because all fixed costs are not deducted from revenue, unless all of the company's manufactured goods are sold. In addition to skewing a profit and loss statement, this can mislead management.

- Since absorbing costing emphasizes total cost (both variable and fixed) it is not useful for management to use it to make decisions for operational efficiency, or to control or plan.

- It does not provide as good of a cost and volume analysis as direct costing does. If fixed costs are an especially large part of total production costs, it is difficult to determine the variations in costs that occur at different levels of production..

- Since absorbing costing includes overhead, it is unfavorable when compared to direct costing when making incremental pricing decisions. Direct costing only includes the extra costs of producing the next incremental unit of a product.

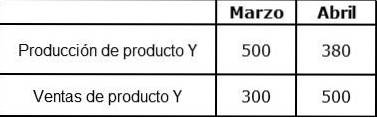

Organization X only produces and sells product Y. The following financial information is known about product Y:

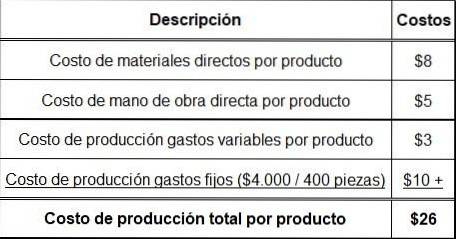

Selling price per piece: $ 50.

Direct material costs per product: $ 8.

Direct labor costs per product: $ 5.

Variable production overhead costs per product: $ 3.

There was no initial stock in March. Fixed overhead costs are now budgeted at $ 4000 per month and have been absorbed by production. A regular production is 400 pieces per month.

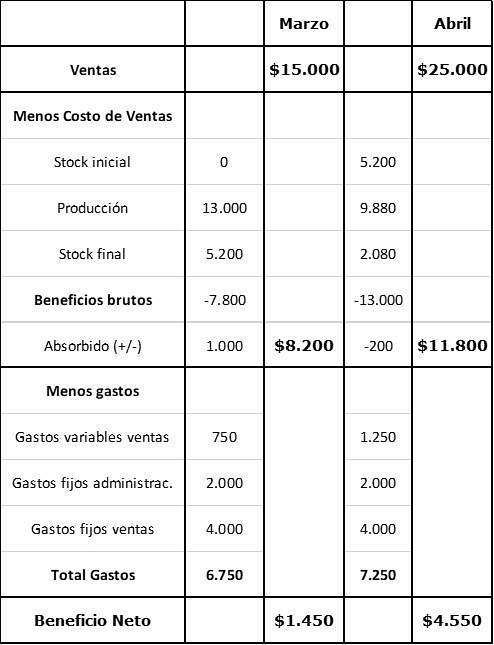

The additional costs are:

- Fixed costs per sales: $ 4000 per month.

- Fixed administration costs: $ 2000 per month.

- Variable sales costs (commission): 5% of sales revenue.

Yet No Comments