The joint costs, in accounting, they are the costs incurred in a joint production process. Joint costs may include direct material costs, direct labor, and manufacturing overhead..

A joint process is a production process in which one input produces multiple outputs. It is a process in which when looking for the output of a product type to be created, other types of products are also automatically created.

Manufacturers incur many costs in the production process. The job of the cost accountant is to track these costs on a certain product or process (cost object) during production.

Some costs cannot be assigned to a single cost object, as these costs favor more than one product or process over the course of manufacturing. These costs are the so-called joint costs.

Understanding the full scope of the concept of joint costs helps accountants and managers know which departments to charge for costs incurred.

Article index

A joint cost is an expense that favors more than one product, and for which it is not possible to separate the contribution to each product. The accountant must determine a consistent method for assigning joint costs to products.

Companies that produce more than one product must understand accounting concepts, such as joint and common costs. These theories demonstrate differences in cost allocation and help companies accurately forecast costs and profits..

Almost all manufacturers incur joint costs at some level in the manufacturing process. It can also be defined as the operating cost of joint production processes, including waste disposal.

Joint costs are likely to occur to some extent at different points in any manufacturing process.

It is essential to assign the joint cost to the different joint products manufactured, in order to determine the costs of the individual products.

Joint processes are production processes in which the creation of one product also simultaneously creates other products. It is a process in which one input produces multiple outputs.

The joint cost becomes useful when the expenses simultaneously favor two or more departments of a company. As such, the accounting department must allocate twice the cost, in the proper proportion, to the appropriate departments..

Joint costing is a useful tool to foster budget cooperation between departments.

It is not always possible to precisely separate the cost or contribution among the beneficiaries, but the joint cost is an acceptable way of accounting in most companies.

To allocate costs to joint products, cost accountants use one of several cost allocation methods.

Joint costs are assigned to joint products based on the quantity produced of each product with respect to total production, taking a physical measure such as weight, units, volume, length, or some other measure that is appropriate for the volume of goods. production.

The physical measurement method for joint cost allocation can be represented in the following formula:

Cost assigned to a joint product = (Quantity produced of the product × Total joint costs) / Quantity of total production

This method is suitable when the physical quantity produced of the joint products accurately reflects their costs..

For example, using the physical measurement method, costs can be assigned to different shades of a paint obtained in a single process..

This method allocates joint costs based on the estimated sale value of a joint product, determined based on the sales value of the total joint production. This is illustrated in the following formula:

Cost assigned to a joint product= (Sales value of product × Total joint costs) / Sales value of total production

This method is suitable when the physical quantity produced of the joint products does not reflect their value, and a reliable estimate of their sales value can be made..

For products that require further processing, the net realizable value method is more appropriate because it takes into account the additional costs required to process and sell the joint products. Under this method, the joint cost is assigned to the products using the following formula:

Cost assigned to a joint product= (VNR of product × Total joint costs) / VNR of total production

where VNR= Estimated sale value - Estimated cost of the additional process.

When such products are further processed after separation, your total costs will also include a higher processing cost..

Let's consider a poultry plant. The plant takes live chickens and turns them into chicken parts used for food. Chickens produce breasts, wings, livers, thighs, and other parts that are used for human consumption.

Similarly, consider an oil refinery. The refinery takes the crude oil and refines it into a substance that can be used for gasoline, motor oil, heating oil, or kerosene..

All of these various products come from a single input: crude oil. In both examples, a single input produces multiple outputs. These are both examples of joint production processes.

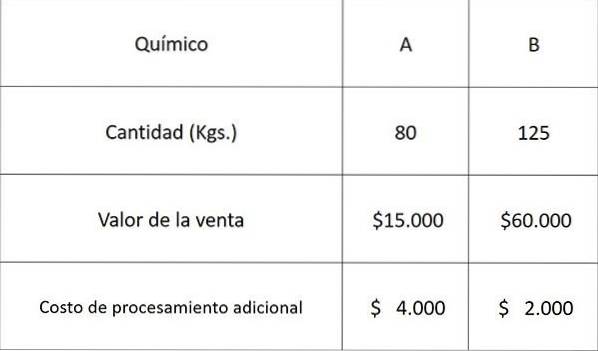

Let's use the following data related to two chemicals A and B obtained from a joint process and assign the joint costs using each of the above methods.

The total manufacturing cost of the joint process was $ 30,000.

The cost to be assigned to chemical A would be:

By physical measurement method: 80 × 30,000 ÷ (80 + 125) = $ 11,707

Relative value of sales method: 15,000 × 30,000 ÷ (15,000 + 60,000) = $ 6,000

VNR method: 11,000 × 30,000 ÷ (11,000 + 58,000) = $ 4,783

where 11,000 = 15,000 - 4,000 and 58,000 = 60,000 - 2,000

Taking the estimated cost of chemical A and since there are only two products, the cost to be assigned to chemical B can be calculated by simply subtracting the above costs from the total, for each respective method, as shown below:

By physical measurement method: 30,000- 11,707 = $ 18,293

Relative value of sales method: 30,000- 6,000 = $ 24,000

VNR method: 30,000- 4,783 = $ 25,217

Yet No Comments