The cost statement or the cost sheet is a breakdown of all the costs that have been incurred during a given period of time. It is made up of direct and indirect costs.

The cost statement is the largest cost in the income statement and shows the cost of the products. The cost to retailers and wholesalers is the amount that has been paid during the period.

The process for calculating the cost for manufacturers is more complex and has many components: direct materials, direct labor, factory and administration overhead, and sales and distribution overhead..

In a store, the inventory value is calculated just by looking at the supplier's invoice. In a manufacturing factory, the value of inventory is calculated by computing how much it costs to make the products.

So to calculate how much the inventory is worth, you need to calculate how much it costs to manufacture the finished products. These manufacturing costs and calculations are displayed on the cost statement.

Article index

The cost of manufactured goods statement supports the cost of merchandise sold figure in the income statement. The two most important numbers in this state are the total cost of manufacture and the cost of manufactured goods..

Total manufacturing cost includes the costs of all resources put into production during the period. That is, direct materials, direct labor, and applied overhead.

The cost of manufactured goods consists of the cost of all finished goods during the period. Includes total manufacturing cost plus beginning process inventory balance minus ending process inventory balance.

The cost of merchandise sold is the cost of all products sold during the period, and includes the cost of finished products plus the beginning inventory of finished products minus the ending inventory of finished products..

The cost of merchandise sold is reported as an expense in the income statements. Manufacturing costs are as follows:

They are the materials used directly in the manufacture of the product. It is also known as a raw material. For example, the wood used to make tables or furniture.

It is the labor involved directly in the manufacture of the product. This includes people working manually or operating the machines used to make the product..

They are general business expenses attributable to the manufacture of the product. Includes the rental of the factory plant, insurance for the factory plant or machines, water and electricity specifically for the factory plant.

If a business had a plant and also an office building, where the administrative work is done, these overheads would not include any of the expenses to run the office building, only the factory expenses.

They are the inventories that are used in the manufacturing process, but whose cost is negligible. For example, to make a car, the screws, nuts and bolts would be indirect materials.

Cleaning materials consumed when producing a completed clean car would also be indirect materials.

Indirect materials are recorded separately from direct materials. They are included in the category of overhead.

It is the cost of the personnel who are not directly involved in the manufacture of the product, but whose cost is part of the factory's expenses.

Included are the salaries of factory supervisors, cleaners and security guards.

Indirect labor is recorded separately from direct labor. Like indirect materials, it is included in overhead.

To calculate the value of direct materials used in the manufacturing process, the following is done:

The beginning balance of the direct materials inventory is added to the purchases made during the accounting period. The ending balance of the direct materials inventory is subtracted from that amount. The result will be the cost of the direct materials used.

Direct materials cost used = direct materials inventory beginning balance + direct materials purchases - direct materials inventory ending balance.

The wages paid to the labor, along with any other direct charges, are then added to the cost of the direct materials used. This will be the primary cost.

Primary cost = direct labor cost + cost of direct materials used.

Factory overhead is collected, which includes rent, utilities, indirect labor, indirect materials, insurance, property taxes, and depreciation.

Then add the primary cost, factory overhead, and the beginning balance of work in process at the beginning of the accounting period. The final balance of the work in process is subtracted, resulting in the cost of the manufactured products.

Cost of manufactured products = primary cost + factory overheads + initial balance of works in process - final balance of works in process.

The beginning balance of finished goods inventory is then added to the cost of manufactured goods to obtain the cost of goods available for sale..

Cost of products available for sale = beginning balance of finished products inventory + cost of manufactured products.

The closing balance of finished goods inventory at the end of the accounting period is subtracted from the cost of products available for sale. This is the cost of the merchandise sold.

Cost of merchandise sold = cost of products available for sale - final balance of finished products inventory.

Selling and distribution overhead expenses are listed, such as sales staff salary, travel expenses, advertising, and sales taxes. These overheads are added to the cost of merchandise sold, resulting in cost of sales, or total cost at the end of the cost statement..

Non-product related expenses such as donations or fire losses are not included.

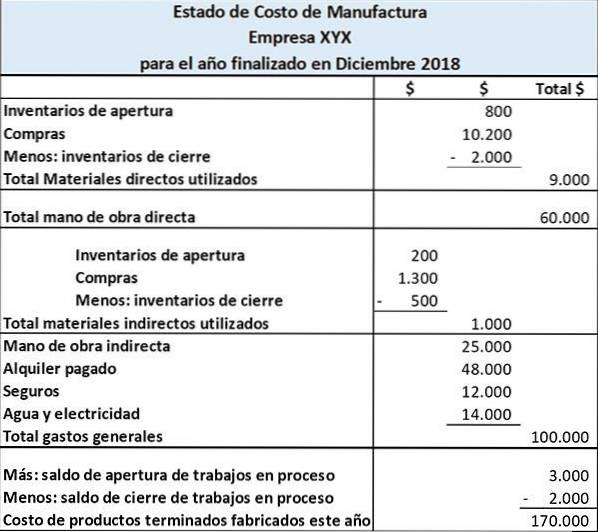

The Farside Manufacturing Company makes calendars and books. The cost statement of manufactured products is as follows:

This statement shows the costs incurred for direct materials, direct labor, and manufacturing overhead. The state totals these three costs to have the total cost of manufacture during the period.

By adding the beginning balance of the process inventory and subtracting the ending balance of the process inventory from the total manufacturing cost, we obtain the cost of the finished products manufactured..

Yet No Comments