The integral percent method It is one of the techniques used for the vertical analysis of financial statements. With this method you can prepare an analysis of the financial structure of a company for a certain period.

It consists of a representation of the standard headings in a financial statement, which are expressed as a percentage of a base heading. Used to show the relative sizes of different accounts in a financial statement.

It is carried out by taking the amount of the most significant heading of the financial statement, comparing with this all the other individual items of the statement. It is also known as the percent reduction method or the common percent method..

When using this method of analysis, each line in a financial statement is analyzed as a percentage of another line. Therefore, it is a proportional analysis method.

Article index

This method is excellent for showing what is happening within a company's financial statements. However, it cannot answer the most important question of any analysis: Why?

For example, with this method of analysis it could be clearly seen that the cost of merchandise sold is a major reason why profits are declining, despite a company's strong sales growth..

However, what cannot be known from vertical analysis is why that happens. Did the costs increase? Did management cut prices? Was it a bit of both? Percent-Integral Analysis Raises These Questions, but Cannot Provide the Answers.

The integral percent method helps to better understand the composition of a financial statement. It can also be very effective in understanding key trends over time. In this method, both assets and liabilities could be considered equal to 100%.

For example, on the balance sheet the company's total assets will show as 100%, and all other accounts, both on the asset and liability sides, will show as a percentage of the total amount of assets..

By doing this every year, you will create an appreciation of the change in the distribution of total assets..

This method is also often used to compare companies of different sizes with each other, in the form of a benchmarking.

It can be difficult to compare the balance sheet of a $ 1 billion company to that of a $ 100 billion company. Common-size vertical analysis accounts allow significant comparison and contrast of quantities of very different magnitudes.

Because the same headings appear in any organization, this makes it easy to compare companies. For example, comparing borrowed capital versus total assets.

The percent-integral method is also the most effective way to compare a company's financial statements to industry averages..

Using actual dollar amounts would be ineffective when analyzing an entire industry, but percentages, which are of a common size, solve that problem and make comparison with the industry possible..

This method can also be applied to the income statement accounts. For example, the sales amount for the first line will be displayed as 100%, and all other accounts will be displayed as a percentage of the total number of sales..

By representing the standard headings as a percentage of the total turnover for that year, it is easy to obtain information about the distribution of the money obtained with the different costs, expenses and profits..

You can see how these contribute to profit margins and if profitability is improving over time. This allows successive years to be compared to identify certain trends. In addition, it is easier to compare the profitability of a company with its peers..

To perform a balance sheet analysis with the whole percent method, total assets, total stockholders' equity, and liabilities are generally used as base amounts..

On the other hand, all assets individually, or if the condensed balance sheet is used, groups of assets are expressed as a percentage of total assets..

Shares, long-term debts and current liabilities are expressed as a percentage of total equity and liabilities.

To perform an analysis of the income statement with this method, the sales amount is generally used as the basis.

On the other hand, all other components of the income statement, such as cost of goods sold, gross profit, operating expenses, income tax and net profit, etc., are shown as a percentage of sales. The percentage is calculated using the following formula:

Integral Percent = (Amount of individual item / Amount of base value) x 100

A basic percent-integral analysis only needs a single statement for one period. However, comparative statements can be prepared to increase the usefulness of the analysis..

When total assets are used in the denominator, each balance sheet item is viewed as a percentage of total assets..

For example, if total assets equal $ 500,000 and accounts receivable is $ 75,000, accounts receivable represent 15% of total assets..

If accounts payable total $ 60,000, accounts payable is 12% of total assets.

You can see how much debt the company has in proportion to its assets. Also, how short-term debt directly compares to current assets.

The higher the proportion of current assets, the stronger the company's working capital position and the ability to meet short-term obligations.

When these percentages are compared to numbers from the previous year, trends can be seen and a clearer understanding of the financial direction in which the company is headed can be developed..

If investment in assets is increasing, but owner's equity is shrinking, then too much of the owners' equity is being taken or profitability is falling.

The latter could mean that assets are not being used wisely and operational changes need to be made. Such comparisons help identify problems for which the underlying cause can be found and corrective action taken..

While total assets are used as the basis for vertical balance sheet analysis, the denominator can also be changed, depending on where it is on the balance sheet..

Total liabilities are used to compare all liabilities and total equity to compare all equity accounts.

For example, the short-term debt is $ 50,000 and the total liability is $ 200,000. Therefore, short-term debt is 25% of total liabilities. Comparing these numbers to historical figures can help detect sudden changes.

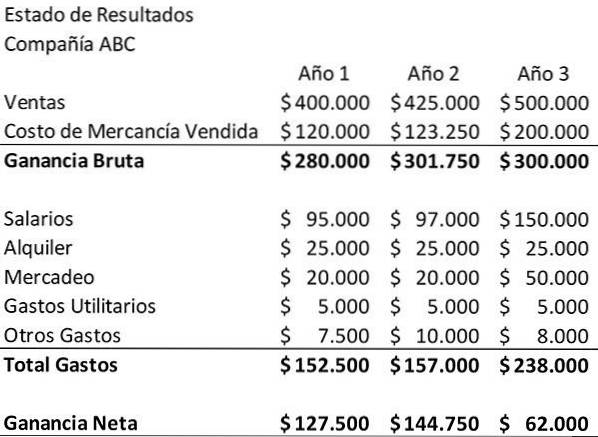

The example below shows the income statement for Company ABC for a three-year period. This will be used as a starting point for doing a vertical analysis..

First, the income statements should be reviewed as they are presented in dollar terms. The company's sales have grown during this period. On the other hand, net income fell considerably in the third year.

Salaries and marketing expenses have increased, which is logical given the increase in sales. However, these expenses do not appear, in principle, large enough to explain the decrease in net income. To see exactly what is going on, you have to dig deeper.

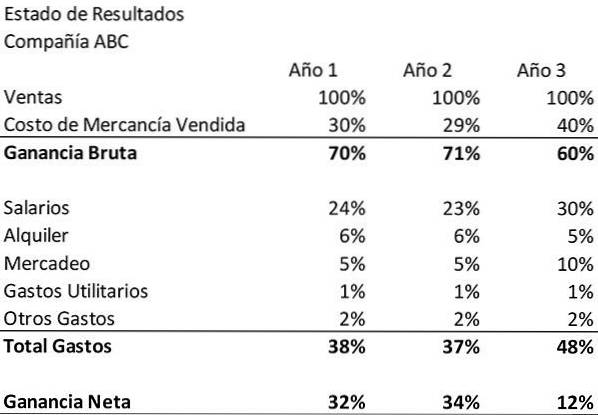

To do this, a “common-size income statement” will be created and the percent-integral method will be applied. For each account in the income statement, divide the amount given by the company's sales for that year.

Doing this will create a new income statement showing each account as a percentage of sales for that year.

As an example, in the first year the company's "Salaries" expense, $ 95,000, will be divided by its sales for that year, $ 400,000. That result, 24%, will appear in the vertical analysis table next to Salaries for the first year. This is how the table should look when completed.

The integral percent method confirms what is already observed in the initial review of the income statement. It also reveals the missing factor in ABC Company's decline in net income: the cost of merchandise sold..

First, it can be seen that the company's marketing expenses increased not only in terms of money, but also as a percentage of sales..

This implies that the new money invested in marketing was not as effective in driving sales growth as in previous years. Wages also grew as a percentage of sales.

This method also shows that in years one and two, the company's products cost 30% and 29% of sales to produce, respectively..

In the third year, however, the cost of merchandise sold soared to 40% of sales. That's driving a significant decline in gross profit..

This change could be due to higher expenses in the production process, or it could represent lower prices..

You cannot be sure without knowing about the management of the company. However, with this method it can be seen clearly and quickly that ABC Company's cost of merchandise sold and gross profit are a big problem..

Yet No Comments