The net present value (NPV) is the difference between the present value of cash inflows and the present value of cash outflows during a given period of time.

Net present value is determined by calculating costs (negative cash flows) and benefits (positive cash flows) for each period of an investment. The period is usually one year, but could be measured in quarters or months.

It is the calculation used to find the present value of a future flow of payments. It represents the value of money over time and can be used to compare investment alternatives that are similar. Any project or investment with a negative NPV should be avoided.

Article index

The time value of money determines that time affects the value of cash flows.

For example, a lender may offer 99 cents for the promise of receiving $ 1 the next month. However, the promise of receiving that same dollar 20 years from now would be worth much less to that same lender today, even if the payoff in both cases were equally true..

This decrease in the present value of future cash flows is based on the chosen rate of return, or discount rate..

For example, if there is a series of identical cash flows over time, the current cash flow is the most valuable, and each future cash flow becomes less valuable than the previous cash flow..

This is because the present flow can be reversed immediately and thus begin to obtain profitability, while with a future flow you cannot.

Because of its simplicity, net present value is a useful tool for determining whether a project or investment will result in a net profit or loss. A positive net present value results in profit, while a negative one results in a loss.

Net present value measures the excess or deficit of cash flows, in terms of present value, above the cost of funds. In a theoretical budget situation with unlimited capital, a company should make all investments with a positive net present value.

Net present value is a central tool in cash flow analysis and is a standard method for using time value of money to evaluate long-term projects. It is widely used in economics, finance and accounting.

Used in capital budgeting and investment planning to analyze the profitability of a planned investment or project.

Suppose an investor could choose to receive a payment of $ 100 today or in one year. A rational investor would not be willing to postpone payment.

However, what if an investor could choose to receive $ 100 today or $ 105 in a year? If the payer is trustworthy, that extra 5% might be worth the wait, but only if there was nothing else investors could do with the $ 100 that earned more than 5%..

An investor might be willing to wait a year to earn an additional 5%, but that may not be acceptable to all investors. In this case, 5% is the discount rate that will vary depending on the investor.

If an investor knew they could earn 8% of a relatively safe investment over the next year, they would not be willing to postpone paying 5%. In this case, the investor's discount rate is 8%.

A company can determine the discount rate using the expected profitability of other projects with a similar level of risk, or the cost of borrowing money to finance the project..

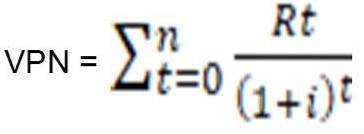

To calculate the net present value, the following formula is used, shown below:

Rt = net inflow or outflow of cash in a single period t.

i = discount rate or return that could be obtained on alternative investments.

t = number of time periods.

This is an easier way to remember the concept: NPV = (Present value of expected cash flows) - (Present value of cash invested)

In addition to the formula itself, the net present value can be calculated using tables, spreadsheets, or calculators..

Money in the present is worth more than the same amount in the future, due to inflation and the gains from alternate investments that could be made during the time in between.

In other words, a dollar earned in the future will not be worth as much as one earned in the present. The discount rate element of the net present value formula is one way to take this into account.

- Take into account the value of money over time, emphasizing previous cash flows.

- Look at all the cash flows involved throughout the life of the project.

- Using the discount reduces the impact of less likely long-term cash flows.

- Has a decision-making mechanism: reject projects with negative net present value.

Net present value is an indicator of how much value an investment or project adds to the business. In financial theory, if there is a choice between two mutually exclusive alternatives, the one that produces the highest net present value should be selected..

Projects with adequate risk may be accepted if they have a positive net present value. This does not necessarily mean that they should be carried out, since the net present value at cost of capital may not take into account the opportunity cost, that is, the comparison with other available investments..

An investment with a positive net present value is assumed to be profitable, and an investment with a negative one will result in a net loss. This concept is the basis of the net present value rule, which states that only investments with positive NPV values should be considered..

A positive net present value indicates that the planned earnings that are generated by a project or investment, in present dollars, exceed the projected costs, also in present dollars..

One drawback of using a net present value analysis is that it makes assumptions about future events that may not be reliable. Measuring the profitability of an investment with net present value is largely based on estimates, so there can be a substantial margin for error.

Estimated factors include investment cost, discount rate, and expected returns. A project may require unforeseen expenses to get started or may require additional expenses at the end of the project.

The payback period, or payback method, is a simpler alternative to net present value. This method calculates the time it will take for the original investment to be repaid.

However, this method does not take into account the time value of money. For this reason, payback periods calculated for long-term investments have greater potential for inaccuracy..

Also, the payback period is strictly limited to the amount of time required to recoup the initial investment costs. The rate of return on investment may experience sudden movements.

Comparisons using payback periods do not take into account the long-term returns of alternate investments.

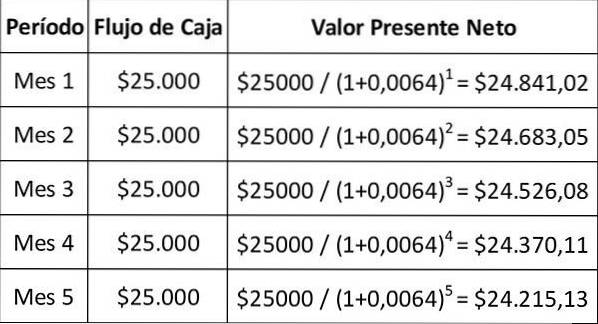

Suppose that a company can invest in equipment that will cost $ 1,000,000, and is expected to generate income of $ 25,000 per month for 5 years.

The company has the capital available for the team. Alternatively, you could invest it in the stock market to get an expected return of 8% per annum..

Managers feel that buying equipment or investing in the stock market are similar risks.

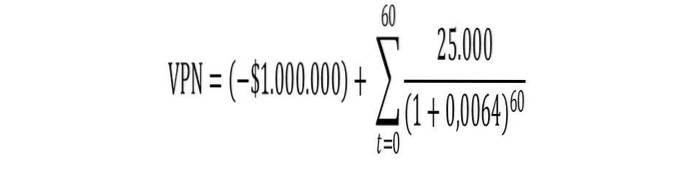

Since the equipment is paid for in advance, this is the first cash flow included in the calculation. There is no elapsed time that needs to be accounted for, so the $ 1,000,000 output does not need to be discounted.

The team is expected to generate a monthly cash flow and last for 5 years. This means that there will be 60 cash flows and 60 periods included in the calculation..

The alternate investment is expected to pay 8% per annum. However, because the equipment generates a monthly cash flow, the annual discount rate must be converted to a monthly rate. Using the following formula, it is found that:

Monthly discount rate = ((1 + 0.08)1/12) -1 = 0.64%.

Monthly cash flows are obtained at the end of the month. The first payment arrives exactly one month after purchasing the equipment.

This is a future payment, so it must be adjusted for time value of money. To illustrate the concept, the table below discounts the first five payments.

The complete calculation of the net present value is equal to the present value of the 60 future cash flows, less the investment of $ 1,000,000.

The calculation could be more complicated if the equipment was expected to have some value at the end of its useful life. However, in this example, it is not supposed to be worth anything.

This formula can be simplified to the following calculation: NPV = (- $ 1,000,000) + ($ 1,242,322.82) = $ 242,322.82

In this case, the net present value is positive. Therefore, the equipment must be purchased. If the present value of these cash flows had been negative because the discount rate was higher, or the net cash flows were lower, the investment would have been avoided..

Yet No Comments