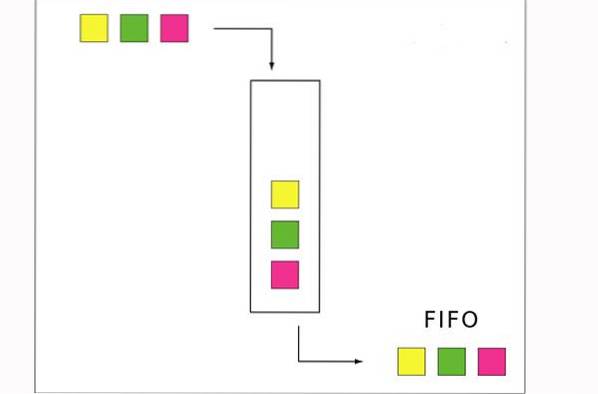

The FIFO method is an inventory valuation technique whose initials correspond to "First In, First Out" (first in, first out). It assumes that the cost flow is based on the fact that the first products purchased are also the first products that are sold..

In most companies this assumption coincides with the actual flow of products, which is why it is considered the most correct inventory valuation method in theory. The FIFO flow concept makes sense for a business to follow as selling the oldest products first reduces the risk of inventory obsolescence.

The FIFO method is permitted under Generally Accepted Accounting Principles and International Financial Reporting Standards. This method provides the same results under the periodic or permanent inventory system..

The accounting method that a company decides to use to determine the costs of its inventory can directly affect the balance sheet, the income statement and the cash flow statement..

Article index

Under the FIFO method, the first products purchased are the first to be removed from the inventory account. This causes the remaining products in inventory to be accounted for at the most recently incurred costs..

In this way, the inventory asset recorded on the balance sheet will contain costs quite close to the most recent costs that could be obtained in the market..

However, this method also causes older historical costs to be compared to current revenues, as they are recorded in the cost of merchandise sold. This means that the gross profit margin does not necessarily reflect an appropriate mix between income and costs..

If prices are going up, FIFO gives us a better indication of the ending inventory value on the balance sheet, but it also increases net income, because inventory that could be several years old is used to value the cost of merchandise sold..

Inventory is assigned costs as items are prepared to be sold. These allocated costs for FIFO are based on what came first. For example, if 100 items were purchased for $ 10 and then 100 more items were purchased for $ 15, FIFO will assign the cost of the first item resold to $ 10.

After selling 100 items, the new cost of the item will become $ 15, regardless of any additional inventory purchases made.

The FIFO method follows the logic that to avoid obsolescence, a business would sell the oldest items in inventory first and keep the newest items in inventory..

If a business sells perishable items and sells the oldest items first, FIFO will give the most accurate estimate of its inventory and sales profit. This includes retail businesses that sell food or other products with an expiration date, such as medicines..

However, even companies that do not fit this description may want to use this method for the following reason: According to FIFO, inventory left on the shelf at the end of the month is valued at a cost closer to what is the current price of those articles.

This would generate a robust balance sheet report, because assets would potentially have a higher value under the FIFO method than they would under the LIFO method..

The profit and loss report would also reflect a higher profit under the FIFO method. Although this could result in higher taxes, it is possible to consider using this method because it would show a stronger financial position for potential investors and lenders..

- FIFO results in a lower cost of merchandise sold. This is due to the fact that older items generally tend to have a lower cost than more recently purchased items, due to possible price increases..

- A lower value of the cost of merchandise sold will result in a greater profit for the company.

- A higher tax bill. Because FIFO produces a higher profit, more taxes will likely be paid as a result.

- There is no guarantee that older items will be sold first, which could cause the product to reach its expiration date before it is sold.

This is something that many grocery stores experience, with customers pulling merchandise from the back rather than the front of the shelf..

The FIFO method assumes that the first unit that enters inventory is the first that is sold.

For example, suppose a bakery produces 200 loaves on Monday at a cost of $ 1 each. Tuesday produces 200 more loaves, but at a cost of $ 1.25 each.

The FIFO method establishes that if the bakery sells 200 loaves on Wednesday, the cost of this merchandise sold will be $ 1 per loaf, for a total of $ 200, which is recorded in the income statement, because that was the cost of each one. of the first 200 loaves in inventory.

The loaves produced at $ 1.25 are then assigned to ending inventory, which appears on the balance sheet, at a cost of 200 x $ 1.25 = $ 250..

If inflation did not exist, then all three inventory valuation methods would produce exactly the same results. When prices are stable, the bakery will be able to produce all of its loaves for $ 1, and FIFO, LIFO, and average cost will cost $ 1 per loaf..

For example, suppose a grocery store receives 50 units of milk on Monday, Wednesday, and Friday. If you walk into that store on Friday to buy a gallon of milk, the milk you buy will most likely come off Monday delivery. This is because that's what was put on the shelf first.

Using the FIFO inventory method, the store would correlate all milk sales with what was received on Monday until 50 units are depleted. It would be done even if a customer comes to the back and takes a cooler carton.

This may sound nuanced, but it becomes very important when prices fluctuate from the supplier. For example, if what was received on Wednesday costs more than what was received on Monday, due to inflation or market fluctuations.

Yet No Comments