The LIFO and FIFO methods are valuation methods used in accounting for inventory management and in financial matters related to the amount of money that a company must have tied to the inventories of finished products, raw materials, parts or components.

How a business chooses to account for its inventory can have a direct impact on its balance sheet, the profit shown on its income statement, and its cash flow statement..

Not only do companies have to look at the number of items sold, but they also need to track the cost of each item. Using different methods for calculating inventory costs affects the company's profits. It also affects the amount of taxes you have to pay each year..

These methods are used to handle cost projections related to inventory, restocking (if purchased at different prices), and for various other accounting purposes..

Article index

LIFO and FIFO are cost stratification methods. They are used to value the cost of merchandise sold and the ending inventory. The equation to calculate the ending inventory is as follows:

Ending Inventory = Beginning Inventory + Net Purchases - Cost of Merchandise Sold

The two common methods for valuing this inventory, LIFO and FIFO, can give significantly different results..

The acronym FIFO stands for "First In, First Out", which means that the items that were added to inventory first, the oldest, are the first items to be removed from inventory for sale..

This does not necessarily mean that the oldest physical item is the one to be tracked and sold first. The cost associated with the inventory that was purchased first is the cost that will first be recorded for sale..

In this way, with the FIFO method, the inventory cost reported in the balance sheet represents the inventory cost of the items that were most recently acquired..

Because FIFO represents the cost of recent purchases, it generally more accurately reflects inventory replacement costs..

If costs are increasing, when the first items that entered the inventory are sold first, which are the least expensive, the cost of the merchandise sold is reduced, thus reporting more benefits and, therefore, paying a higher amount of income tax short term.

If costs are decreasing, by selling the first items that entered the inventory first, which are the most expensive, the cost of the merchandise sold increases, thus reporting less profit and, therefore, paying a lower amount of income tax in the short term.

Generally in the FIFO method there are fewer layers of inventory to track, as older layers are continually depleted. This reduces the maintenance of historical records.

Since there are few layers of inventory, and those layers are more reflective of new prices, unusual crashes or spikes in the cost of merchandise sold rarely occur, caused by access to old layers of inventory..

The acronym LIFO stands for “Last In, First Out,” which means that the items most recently added to inventory are considered the first items to be removed from inventory for sale..

If costs are increasing, the last items to enter inventory, which are the most expensive, are sold first, increasing the cost of merchandise sold, thus reporting less profit. Therefore, a lower amount of income tax is paid in the short term..

If costs are decreasing, selling the last items in inventory first, which are the least expensive, reduces the cost of merchandise sold. In this way, more profits are reported and, therefore, a greater amount of income tax is paid in the short term..

In essence, the main reason for using the LIFO method is to defer the payment of income tax in an inflationary environment..

Generally speaking, the LIFO method is not recommended primarily for the following reasons:

- It is not allowed under IFRS. Much of the world is governed by the established IFRS framework.

- There are generally more layers of inventory to track. Older layers can potentially remain in the system for years. This increases the maintenance of historical records.

- Because there are many layers of inventory, some with costs from several years ago that vary substantially from current costs, accessing one of these old layers can cause a drastic increase or decrease in the amount of the cost of merchandise sold.

This inventory method of accounting rarely provides a good representation of the replacement cost of inventory units. This is one of its drawbacks. Also, it may not correspond to the actual physical flow of the items.

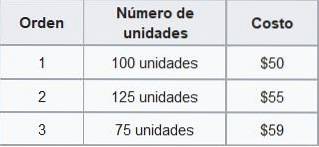

Foo Co. has the following inventory available in November, sorted by date of purchase:

If Foo Co. sells 210 units during November, the company would record the cost associated with selling the first 100 units at $ 50 and the remaining 110 units at $ 55..

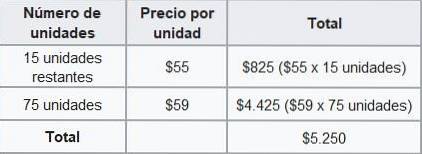

Under the FIFO method, the total cost of sales for November would be $ 11,050 ($ 50 × 100 units + $ 55 × 110 units). The ending inventory will be calculated as follows:

Therefore, the balance sheet would show the ending inventory for November valued at $ 5,250, under the FIFO method..

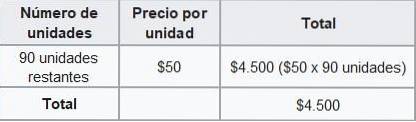

If Foo Co. used the LIFO method, it would pay the cost associated with selling the first 75 units at $ 59, an additional 125 units at $ 55, and the remaining 10 units at $ 50..

Under the LIFO method, the total cost of sales for November would be $ 11,800. The ending inventory will be calculated as follows:

Therefore, the balance sheet would now show the November ending inventory valued at $ 4,500, under the LIFO method..

The difference between the cost of an inventory calculated according to the FIFO and LIFO methods is called the LIFO reserve. In the example above it is $ 750.

This reserve is the amount by which the taxable income of a company is deferred using the LIFO method..

Yet No Comments