Offer is the amount of products and services available in a specific market. The higher the price, the higher the offer.

Demand is the amount of products and services that you are trying to buy in a specific market. The higher the price, the lower the demand.

| Offer | Demand | |

| Definition | Quantity of goods available for sale in a given market, a given period and at a specific price. | Amount of goods that people are willing and able to buy in a given market, for a given period and at a specific price. |

| Influential factors |

|

|

| Theoretical laws that support them | Law of supply: the higher the price, the higher the supply. | Law of demand: the higher the price, the lower the demand. |

Supply is understood as the amount of goods that producers are willing to place on the market for sale in a given period..

When the product offered has a high price, it is assumed that there will be a higher profit margin, which generates an incentive to increase production.

However, when the price is low, the supply decreases, since there are no profitability incentives.

The amount of products available will depend essentially on the sale price, but also on other related factors, such as the expectation of sale, the viability of production and the freedoms or restrictions of the market, among other factors..

If costs are favorable for production, supply will increase, but if costs are unfavorable, supply will decrease.

For example, the production of many sweets requires sugar, which is essential in the production of the product. If the price of that ingredient goes down, the supply will go up. If the price of sugar rises to such an extent that it becomes unfeasible to buy it, production will decrease, as it will become unprofitable to produce in large quantities.

The use of outdated technology can limit the production of a good, so its supply will be low. On the other hand, innovation and cutting-edge technology generate a simplification of processes that generally contribute to lower production costs, causing the supply to increase, as a greater availability of products is guaranteed in less time..

For example, a company that is dedicated to the manufacture of pants with old machines will have a limited supply compared to another company that does the same, but with updated machines, which allow to create more pieces per hour..

Each country has a regulatory framework for economic activities. Depending on this, and the changes that may arise in this matter, the offer may be affected..

For example, the application of a tax exemption for the automotive industry will generate a greater supply of available automobiles. On the other hand, commercial restrictions that fix a certain price band, will make the supply decrease.

The sale expectation has to do with the amount of goods that are projected to sell in a given period. For this, the relevant market studies are carried out that will give an idea of what can happen.

If the result indicates a positive trend, meaning that the product will be sold, steps will probably be taken to increase production when necessary. But if the projection is negative, the offer will decrease to avoid losses.

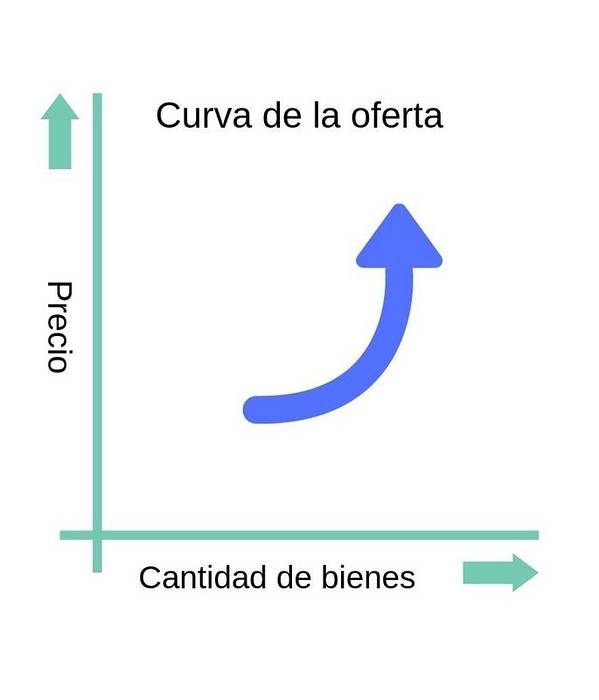

The law of supply is known as the relationship between the demand for a product and the quantity that is available in the market.

This relationship will be mediated by the price of the product and is positive, that is, the higher the price, the higher the availability..

It is a graphic representation that is used to illustrate the relationship between the number of products available and the sale price.

Usually, the supply curve is represented in a Cartesian plane (x-axis and y-axis) and what is expected to be obtained is an intersection between both variables. If the intersection occurs on an upward curve, it is a positive relationship (higher price, higher supply, therefore, more goods available for sale), and if it is a downward curve, it is a negative relationship (lower price , lower offer).

See also: Microeconomics and macroeconomics

In economics, demand is the amount of goods that people are willing to buy in a given period and at a certain price. Demand can be based on both needs and desire for non-essential goods, but in both cases the buyer's ability to pay influences.

This leads to the need for purchasing capacity so that there can be a real demand.

In addition to price, which is a key factor, there are other variables that influence the demand for a good:

It is understood that the greater the amount of income received, the greater the demand, since they have the resources to pay for goods and services available at a certain price. When the income of the population falls (high levels of unemployment, inflation, etc.), the demand will also fall, since the purchasing power is limited..

The tastes and needs of buyers also determine the demand. In the case of tastes, these can often change influenced by current trends. For example, if a certain model of shoe is fashionable, it is foreseeable that the demand for that product will increase..

Needs have to do with the satisfaction of basic requirements, and although they will always be present (because food and clothing will always have to be bought, for example), they will be guided by priorities. How necessary is it to buy a certain brand of food or replace the heating system before the arrival of winter?

Demand can be affected by demographic factors. For example: a high supply of baby clothes will not be in great demand in a geographic area where older people or singles without children predominate.

Here multiple micro and macro economic factors come into play. The family budget, the possibility of a general salary increase, inflation, the availability of certain raw materials, etc..

When the increase of certain types of food items is announced, the foreseeable thing is that people satisfy their demand before the price rises, that is, there is an increase in demand.

The law of demand says that if the price is high, the demand will be low, and if the price is low, the demand will be high. A classic and close example is that of the signature clothing stores. When a new collection arrives, the prices are very high and the demand decreases. But when discount season rolls around and prices are more affordable, demand for those pieces of clothing increases..

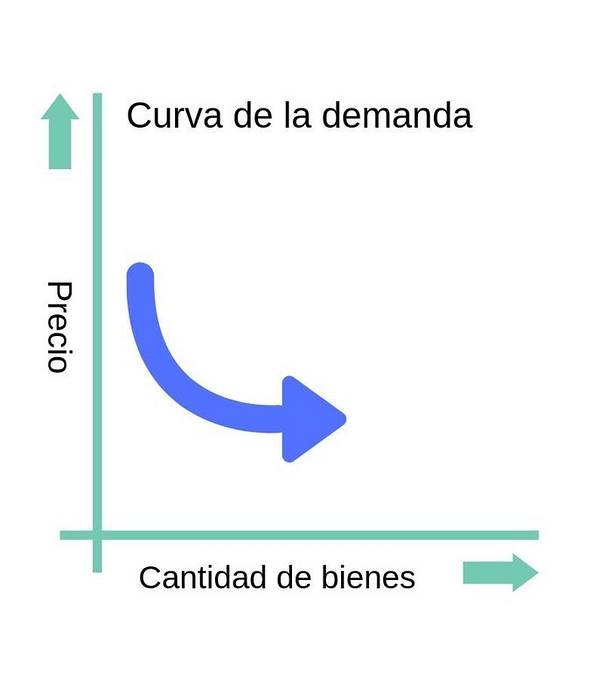

The demand curve is a graphical representation that relates the quantity of goods demanded with a given price. A downward curve on the graph shows that price is inversely proportional to demand. That is, the lower the price, the higher the demand. If the price rises, the quantity of goods that can be purchased decreases.

The law of supply and demand is a model of neoclassical economic theory, which raises the relationship between the price of goods and services and the sales they generate.

Although there is no consensus on the creator of the model, records indicate that the term was first used by the English economist James Steuart Denham in his book Studies of the principles of political economy, published 1776.

This economic model indicates that, in an ideal situation in which companies cannot directly intervene in the price of what they produce (called the market of perfect competition), an equilibrium point will arrive at which a price will be established that will allow the sell everything on offer (emptying the market).

From this it follows that the price of the product will depend on the relationship between the quantity supplied (what is available in the market) and the demand for that product (how many people are willing to pay for it).

The law of supply and demand implies the fulfillment of three requirements:

The law of supply and demand has been criticized because it is assumed in a market of perfect competition, with economic equilibrium and understanding that demand and supply are two independent variables. For critics, by eliminating these assumptions, the model cannot be sustained.

However, the law of supply and demand is still used today to explain the micro and macro economic reality of markets..

See also:

Capitalism and socialism.

Import and export.

Foreign trade and international trade.

Yet No Comments